No Standards, No Limits: How the NBPP 2027 Opens the Door to Silver Spamming

The elimination of standardized plan options removes a structural check on anti-competitive pricing strategies in the ACA marketplace

We are continuing our series analyzing the ruling that came out of the NBPP 2027. In our first post of the series, Wesley covered Cost Sharing Reductions and what the new reporting requirements could mean for how issuers price silver plans; this post takes up a related change: the elimination of the requirement to offer Standardized plan options starting PY 2027. This policy has completed a full cycle, introduced in 2017, discontinued in 2019, revived by a federal court in 2021, reintroduced in 2023, and now eliminated again. Understanding what this could do to plan pricing dynamics within individual rating areas will be an important part of the 2027 rate filing season.

If you shopped for coverage on HealthCare.gov in 2026, you may have noticed that some plans carried a small label reading “easy pricing.” Those were standardized plan options. This is a category of plans that CMS designed at the federal level and required issuers to offer alongside their regular plan lineup.

Standardized plans allow consumers to compare insurance options without having to decode and value slight differences in plan designs. Standardized plans, or “easy pricing” plans, held certain variables constant (like deductible, maximum out of pocket and coinsurance). The comparison then shifts to what differentiates the plans (premium, provider network, formulary, quality ratings.) This was reflected on HealthCare.gov as these Standardized plans were visually flagged noting that the plans shared the same Maximum Out of Pocket (MOOP) values, deductibles, and in-category cost sharing. Consumers could also use a filter to show only standardized plans, effectively hiding the non-standardized options entirely. For a first-time shopper or someone with limited familiarity with health insurance, this was a curated, comparable subset of the market.

For issuers operating in the Federally Facilitated Exchanges (FFE) and State-Based Exchange using the Federal Platform (SBE-FP), standardized options were not optional. Starting in PY 2023, every issuer offering a QHP in the individual market was required to offer a standardized plan option at every metal level, in every product network type, and across every service area where they offered non-standardized plans. The cost sharing parameters for each plan design were published annually by CMS in the Payment Notice rulemaking, so an issuer didn’t design these plans so much as conform to a template CMS specified. The intent was to make it easier for consumers to compare the premium, network and formulary of plans to determine what was best for them. The cost of having to offer these Standardized Plans was borne by the issuers wherever they operated.

Starting in PY 2027, CMS is removing the full regulatory apparatus that created and sustained standardized plan options. The requirement for FFE and SBE-FP issuers to offer these plans has been removed as well as the condition that multiple plans within the same product type, metal level, and service area meaningfully differ from one another has been removed. Additionally, the differentiated display of standardized plans on HealthCare.gov will be eliminated.

Each issuer faces a choice about what to do with their existing Standardized plans. An issuer can keep the plan as-is. If the cost sharing structure stays the same and the plan retains its existing plan ID, enrollees will be auto renewed into it just as they would in any other year. An issuer can modify the plan’s cost sharing. If the changes are significant enough to constitute a new plan under the definition at § 144.103, the old plan gets a new plan ID and is treated as discontinued, meaning current enrollees get crosswalked to another plan in accordance with the crosswalk hierarchy (the same process would occur if an issuer decides to discontinue the plan entirely).

States that have enacted their own standardized plan requirements remain subject to those state-level mandates. State Exchanges retain full flexibility to require standardized plans, design their own templates, and display them however they choose on their own enrollment platforms. What will change is that HealthCare.gov and the federal direct enrollment pathway will no longer differentially display any standardized plans.

CMS cited four years of operational experience (PY 2023–2026) in concluding that the standardized plan option regime failed to achieve its stated objectives. They cited actual plan proliferation getting worse because issuers now had to have a standardized plan in addition to their existing plans. Comparing products was supposed to be easier with standardized plans, but since there were now standard and non-standard plans this led to a more complicated evaluation process. The result, in CMS’s view, was a low uptake of the standardized options as consumers still tended to choose on price, network and known brands. The additional administrative cost associated with requiring a standardized plan outweighed what CMS identified as negligible consumer value.

CMS responded to comments about imposing a meaningful difference standard among an issuer’s plans. A meaningful difference standard would require plans offered by the same issuer within the same metal level and service area to differ in a substantive way such as network type, benefit coverage, or formulary. CMS cited a limited number of instances in PY 2026 where the absence of a meaningful difference standard resulted in plan proliferation as their rationale for not implementing this standard. Further, they were concerned that this would add additional administrative burden to issuers and constrain their ability to offer unique plan designs that cater to an issuer’s local market.

CMS seems to be concerned that standardization and meaningful difference standards do little to limit plan proliferation while creating more regulatory requirements for issuers. They are correct in that these requirements add cost and burden to issuers. We would point out that not all issuers are the same and some smaller issuers may welcome standardized plans as these plans can limit larger issuers (those with more ability to shoulder administrative costs) from flooding markets with plans that are intended only to limit competition. In isolation, removing either requirement might be manageable. Together, the absence of both standardized plan requirements and a meaningful difference standard remove a structural restraint on how issuers can design, price and present their silver plan lineup. This strategy is often referred to as Silver Spamming.

Silver spamming occurs when one issuer has numerous silver plan options, with only slight (some might say not meaningful) differences between them and very small price differences.

The reason to do this has to do with HealthCare.gov and how a prospective member searches for a plan. If a plan is undertaking the silver spamming strategy, they are trying to be the lowest cost silver plan and then flood the silver market with many more, slightly different, plan structures at marginally higher prices. The first thing a price-sensitive prospective member searching for a silver plan will do is sort by premium. The silver spamming issuer occupies the first page of results and pushes competitors to page two. If that member has a chronic health condition and wants to ensure that a specific provider is contracted with a specific plan, they may make it to the second page of results. If they are not sick and just want a basic (some might say, standardized) plan in case they need it, they do not usually make it to the second page of results. This is an anti-competitive behavior couched in plan innovation to facilitate consumer choice.

This brings us to the second aspect of the strategy, and ties in with Wesley’s discussion about Cost Sharing Reduction plans: what type of members are these silver spamming strategies likely to attract? If they are not clicking to the second page of search results it is less likely they are looking for a specific network or formulary. They are looking at the total cost of coverage because they are not concerned with ensuring access to a specific specialist or drug.

Someone searching for coverage who earns less than 250% of the FPL is likely to be looking for a silver plan because those are the plans with Cost Sharing Reduction (CSR) variants, thus offering the most value (independent of issuer).

Consider two separate shoppers, one with a chronic condition who already has a provider (the Utilizer). The other knows they can get health insurance for little to no cost and thus is interested in a plan as a safety net in case something happens (the Non-Utilizer). They each go to Healthcare.gov and they see a list of plans, all offered by the same issuer with slight price and design differences (Silver Spam).

a. The Utilizer is more likely to shop beyond the Silver Spamming options. They know they will use the plan during the year and want to ensure it will cover what they need.

b. The Non-Utilizer is less likely to shop beyond the Silver Spamming options. They may not use the plan over the course of the year but since subsidies are paying for it, they are less concerned with benefits.

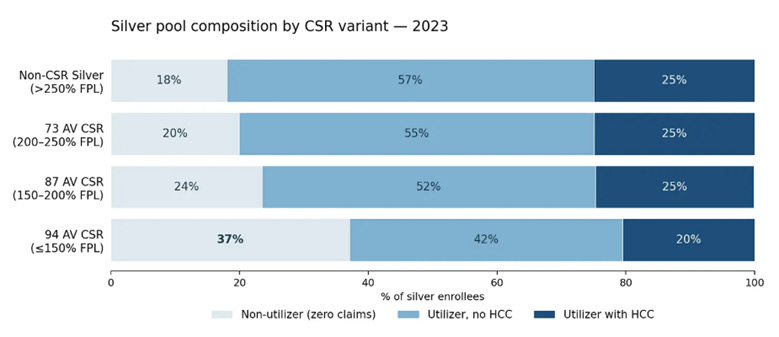

The table below (first shared by Wesley in our first article in this series: Cost Sharing Reductions) illustrates, when the same insurance product becomes less expensive it attracts more Non-Utilizers (or people who do not anticipate utilizing medical services).

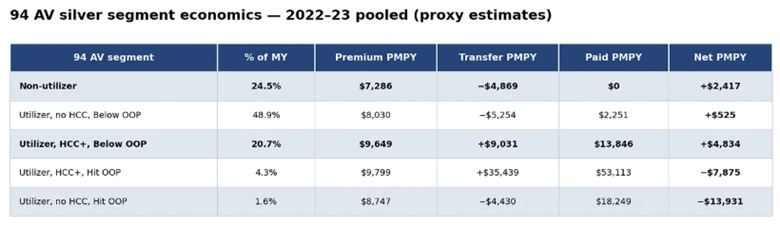

Below is another table from that same piece; here Wesley illustrates the profitability of a member of a 94 AV plan depending on their utilization, HCCs, and out-of-pocket spend mix. It is not a surprise, but if a member does not generate any claims on their health insurance, they are a profitable member, even accounting for a risk adjustment payable.

A Silver Spammer creates multiple similar plans to dominate the first page of Healthcare.gov and thus pick up a disproportionate amount to profitable Non-Utilizers. The issuers that undertake this strategy are trading increased administrative burden to de-risk their membership, but their de-risking means someone else must shoulder more risk.

When one issuer successfully captures a disproportionate share of non-utilizing, price-sensitive silver enrollees, the issuers left behind carry a sicker, higher-utilizing risk pool. Additionally, the Second Lowest Cost Silver Plan (SLCSP) benchmark price is set by the carrier that is expecting to get a larger non-utilizing membership. That benchmark price, which affects all issuers in the rating area, reflects lower claims than what the rest of the issuers in the area are likely to experience. The issuer that was offering a well-designed silver plan with a broad network and a comprehensive formulary now faces a choice between raising premiums to cover their worsening risk mix or exiting the market.

Risk adjustment was designed to be the equalizer in a single pool market like the Affordable Care Act marketplace. If you have sicker members than others in your market, you get risk adjustment from other issuers as compensation. So, if risk adjustment is in place why is Silver Spamming even an issue (outside of the anti-competitive nature of the strategy)? The answer lies in the details of how risk adjustment is calculated.

Part of the Risk Transfer formula includes an Induced Demand Factor (IDF). IDF is designed to account for additional utilization by the same members given richer benefits. We would expect someone who has reached their MOOP to use more benefits because the cost to them is zero. As noted above, this dynamic does not hold when members are lower on the income spectrum and receive highly subsidized plans. These members have a higher proportion of Non-Utilizers. The IDF takes the risk score and factors it up as the expected cost sharing by the member goes down. A Non-Utilizer who bought a CSR 94 variant because it was free to them still has a risk score that is used to determine the risk adjustment associated with their plan as well as the market wide risk score. The result is a risk adjustment market that is over indexed to the Non-Utilizer. This decreased the Utilizers risk score vs the entire market. Thus, the issuers who attracted the Non-Utilizers through a silver spamming strategy pay less into risk adjustment. This would not be an issue if the Utilizers and Non-Utilizers were spread more evenly across the issuers, but because of the spamming the market is comprised of two different utilizer types that behave differently.

These are the fears of what could happen in an environment that does not have Standardized plans and other limiters on an issuer using pricing strategies to push competitors out of the market. We may know as soon as rate filing season if any issuers are planning on using the silver spamming practice, but I suspect many will. Assuming they do, being able to identify it as early as possible to plan around it will be an important part of developing an outlook for PY 2027.

Great piece. Do you think that http://healthcare.gov could make product improvements to prevent silver spamming?

With ARPA subsidies having expired, I would expect the non-utilizers to shift to Bronze plans (or Gold in states with mandated metal relativities) rather than stick to Silver CSR plans. As such, wouldn't a bigger risk be of Bronze Spamming rather than Silver Spamming? This strategy does hurt on the risk adjustment side since Bronze will have the worst AV and IDF factors for non-utilizers, but it still seems the most straightforward way to scoop up healthy membership heavily leveraged on price.